Macroeconomic stability is real, but it is not enough. The challenge of the next decade is to move from an economy that attracts wealth to an economy that produces knowledge, technology and domestic value added.

Co-authors: Nikolaos Antonakakis, Professor of Economics and Director of the School of Business, University of Nicosia, School of Business, Department of Accounting, Economics and Finance, UNIC Athens

Petros Lois, Professor of Accounting and Finance, University of Nicosia, School of Business, Department of Accounting, Economics and Finance, Nicosia

Cyprus has achieved something that should not be underestimated: fiscal consolidation, investment credibility, strong growth and low unemployment. But economic policy is not judged only by whether indicators improve. It is judged by whether a country produces more domestic value, retains the wealth it creates and turns stability into productive resilience.

1. Trap of good numbers

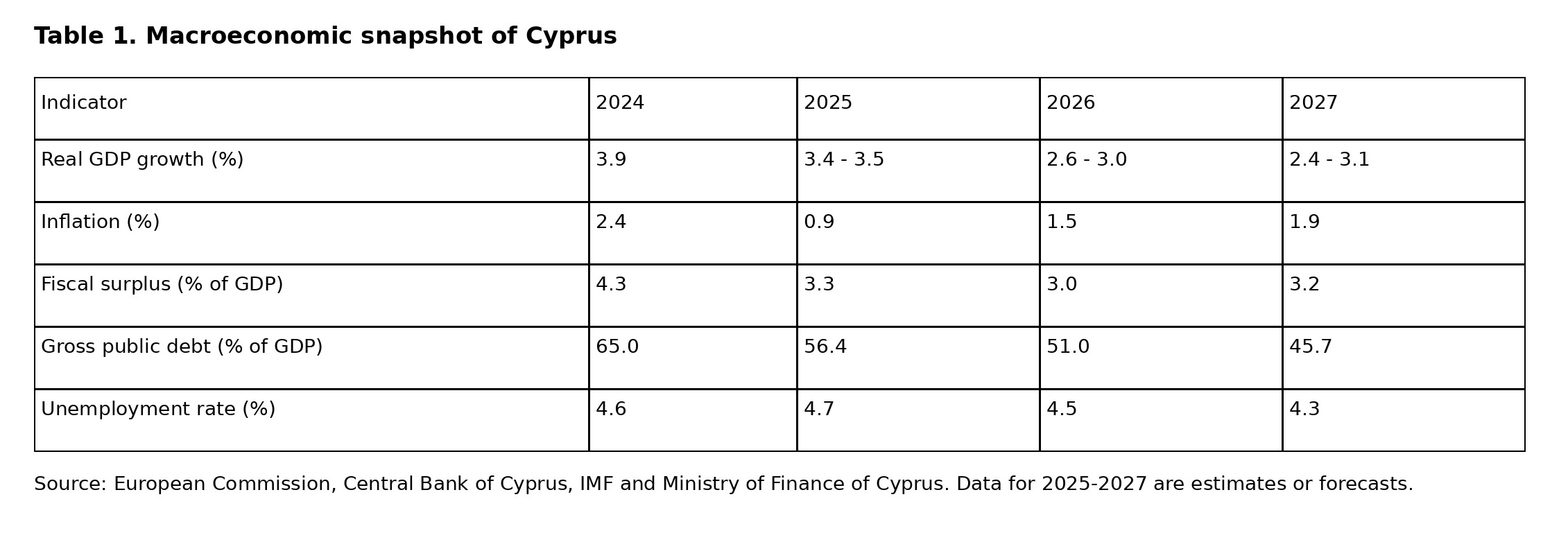

The year 2026 finds the Cypriot economy in a position that, at first sight, appears remarkably strong. Growth remains well above the euro area average, the fiscal balance is still in surplus, public debt is declining at a pace many European economies would envy, and the country has moved away from the period of persistent macroeconomic imbalances. This picture is real. It is not a communication exercise.

Precisely because it is real, however, it becomes dangerous when it turns into complacency. The recovery of macroeconomic indicators does not automatically mean that the productive model has changed. Cyprus may be recording high rates of expansion, but it still operates largely as an economy of services, real estate, consumption and tax attractiveness. In plain terms, GDP is running, but the productive engine remains old fashioned.

The central distinction for 2026 is therefore clear: stabilisation after crisis is not the same thing as building a genuine high value added economy. The first has largely been achieved. The second remains open, difficult and politically demanding.

Indicators do not lie. They simply do not tell the whole truth.

Figure 1. Fiscal repair is impressive, but it does not by itself answer the question of productive upgrading.

2. Growth exists, but real value leaks away

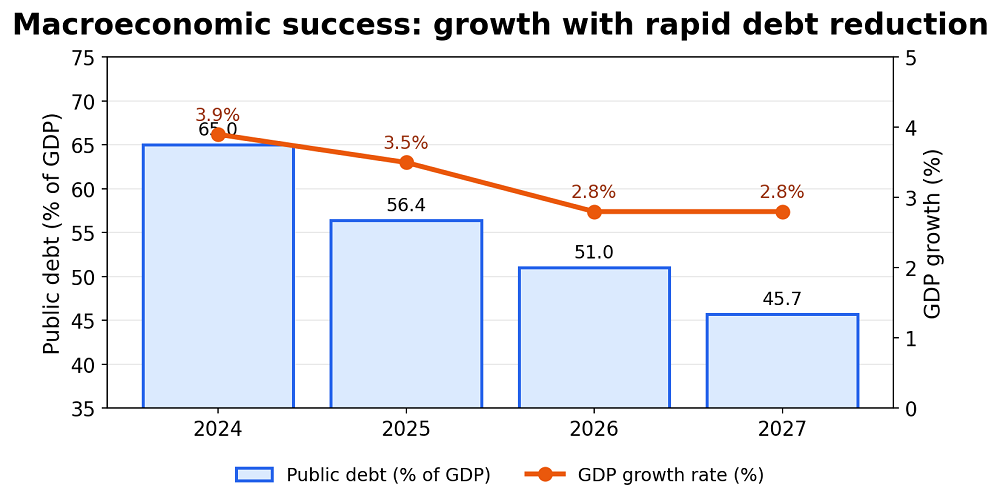

The most revealing mirror of the Cypriot productive model is not GDP, but the balance of payments. It shows whether an economy produces income that remains in the country or whether it functions as a transit space for value. In the case of Cyprus, the answer is mixed. The country exports services successfully, but it imports goods on a large scale and records a substantial outflow of primary income.

The services surplus is impressive. Tourism, shipping, financial services and, above all, telecommunications, computer and information services support the external balance. Yet the goods balance remains deeply negative. Consumption quickly turns into imports because the domestic productive and manufacturing base is narrow.

The deeper problem is the primary income deficit. Foreign owned companies operating in Cyprus increase service exports, employment and tax revenue. At the same time, a significant share of their profits is repatriated to parent companies and shareholders abroad. This creates the familiar gap between Gross Domestic Product and Gross National Income. Put simply, not all the wealth recorded as being produced in Cyprus is wealth that remains in Cyprus.

The conclusion is crucial for market practitioners and policymakers. Attracting foreign companies is not the wrong strategy. The mistake would be to believe that it is sufficient on its own. The objective must be to create deeper linkages with domestic firms, universities, suppliers, technology laboratories and local value chains.

Figure 2. The Cypriot economy has a strong services surplus, but the goods deficit and income outflows limit sustainable national prosperity.

3. Tourism and ICT: two pillars, two different realities

Cyprus does not lack sectors that generate income. It lacks depth, diffusion and productive connection across those sectors. Tourism and ICT reveal this dual reality more clearly than almost any other indicator.

Tourism reached a new historic level in 2025, with more than 4.5 million arrivals and revenues of about 3.7 billion euros. This performance matters. Yet the essential question is not how many more tourists can arrive on an island with limited natural resources. It is how much value each visitor leaves behind. Cyprus needs tourism with higher spending, a longer season, stronger links to local products, culture, education, health, sport and business conferences.

ICT, by contrast, is the most dynamic new sector of the Cypriot economy. The headquartering policy and the relocation of technology companies have created a powerful enclave of outward oriented services. This is where both the major opportunity and the major risk lie.

The opportunity is obvious: income, employment, international networks, expertise and tax revenue. The risk is that Cyprus remains a hospitable platform rather than a co-creator of technology. If domestic SMEs are not connected to multinationals, if universities do not produce applied and marketable knowledge, and if the state does not act as an accelerator of technological upgrading, ICT will remain an enclave economy. It will exist in Cyprus, but it will not sufficiently change Cyprus.

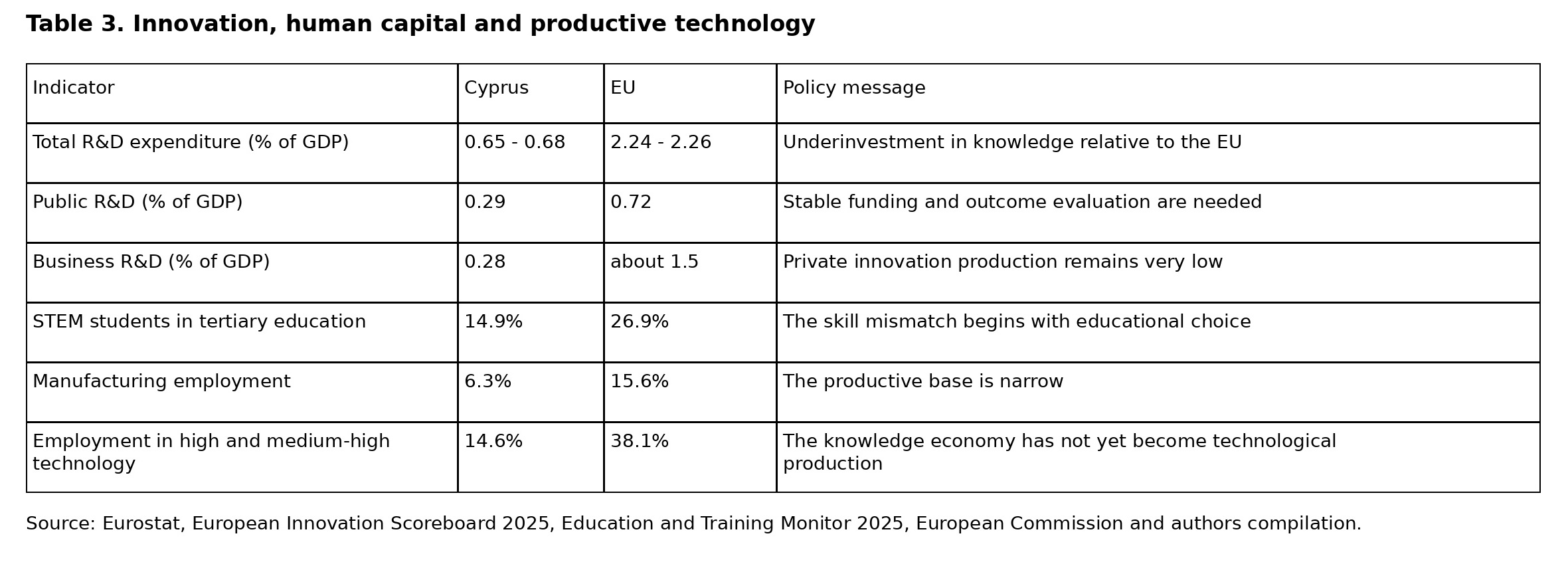

4. Innovation gap is Achilles heel

The most serious weakness of the Cypriot model is not the cyclical dependence on tourism. It is the low capacity to transform knowledge into productive technology. Cyprus has universities, scientific talent, international collaborations and a favourable business environment. It does not yet have a fully functioning chain from research to market.

Research and Development data are revealing. Total R&D intensity is far below the EU average. Public and business R&D remain limited. STEM participation is low, while the manufacturing and technological base of the economy remains narrow. This means the country does not merely have a funding problem. It has a problem of productive architecture.

The market needs data analysts, software engineers, cyber security specialists, energy technicians, network engineers, artificial intelligence specialists and professionals who can bridge technology, management and finance. The education system and training structures are not moving at the same speed. The result is skill mismatch, meaning a market where jobs and people exist, but the skills required by the new productive model are not always there.

In practice, Cyprus needs a modern technology transfer system. Universities must be organically connected to business, research outputs must have a pathway towards patents and spin-offs, SMEs must develop the absorptive capacity to use technology, and the state must evaluate programmes not by absorption of funds, but by measurable productive impact.

Figure 3. Cyprus overperforms in selected knowledge intensive services, but lags in the indicators that build lasting technological production.

5. Energy as permanent tax on production

If innovation is the future of competitiveness, energy is its present. There is no serious strategy for industrial, digital or export upgrading when energy costs operate as a permanent tax on production. Cyprus remains energy isolated, highly dependent on imported fossil fuels and limited in its ability to smooth prices through interconnections or large scale storage.

The data on electricity prices for non-household consumers are especially instructive. In the second half of 2025 Cyprus recorded one of the highest prices in the EU, behind only Ireland. For firms, this means higher operating costs, lower margins, weaker investment capacity and reduced international competitiveness.

The Great Sea Interconnector could become a strategic answer to energy isolation. But the project is not a simple technical matter. It is a geopolitical, financial and regulatory equation of high complexity. Delays, cost concerns and the need for further financial assessment show that the energy transition cannot rely on a single large promise. Cyprus needs a parallel strategy for storage, grids, renewables, energy efficiency and a stable regulatory framework.

Cheaper energy is not only social policy. It is a precondition for productive policy.

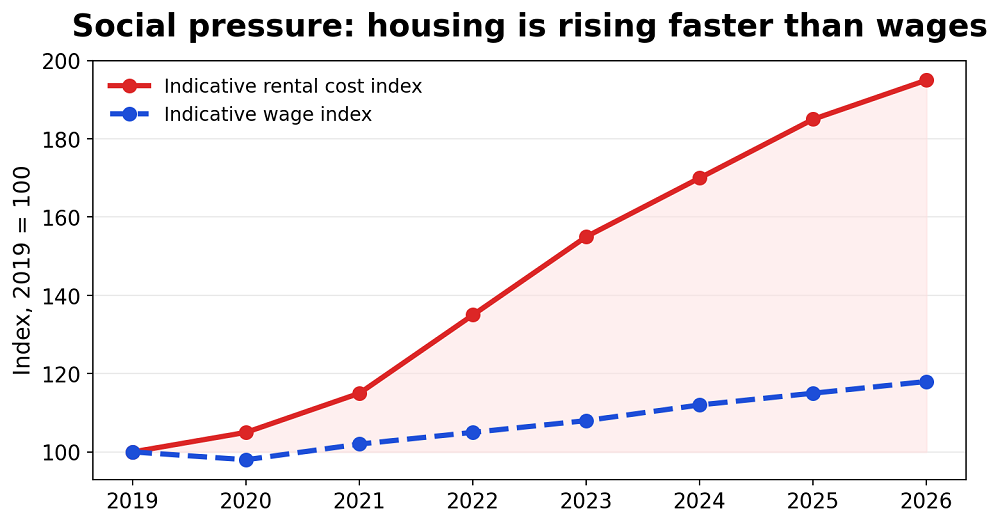

6. Housing cancels part of wage progress

The most immediate social side effect of the current model is housing pressure. The arrival of high income foreign professionals, the concentration of technology firms in specific cities, strong demand for real estate and limited supply of affordable housing have created an environment in which income growth does not always translate into higher real welfare.

For workers, the indicator that matters is not only the wage. It is the wage after rent, energy, transport and basic services. If housing absorbs a disproportionate share of disposable income, even a positive wage development loses much of its social meaning. An economy can grow while large parts of the middle class feel they are not progressing.

This is also the political limit of headquartering when it is not accompanied by housing policy. Attracting high income professionals is not a problem in itself. It becomes a problem when the housing market operates as a mechanism transferring income from local workers to property owners, without sufficient expansion of supply and without social balancing mechanisms.

Figure 4. Indicative representation of the divergence between housing costs and wage developments. The series are presented as index values to illustrate the social pressure.

7. Recovery Fund must not become accounting exercise

The Cyprus Tomorrow plan is one of the last major opportunities to turn European financing into productive transformation. The crucial question is not whether Cyprus will absorb funds. The crucial question is what kind of economy those funds will leave behind.

The experience of many small open economies shows that European programmes are often treated as a cycle of projects, tenders, payments and compliance. This approach is administratively necessary, but strategically insufficient. The Recovery and Resilience Facility should be assessed according to whether it reduces energy costs, accelerates the digital maturity of the state, raises SME productivity, strengthens STEM skills and creates permanent capabilities in applied research.

The partial disbursement of the fifth payment in March 2026 is a reminder that the final phase of the RRF does not tolerate delays. Milestones are not bureaucratic details. They are the mechanism through which the EU asks member states to turn financing into reforms. For Cyprus, 2026 is a year of execution, not merely planning.

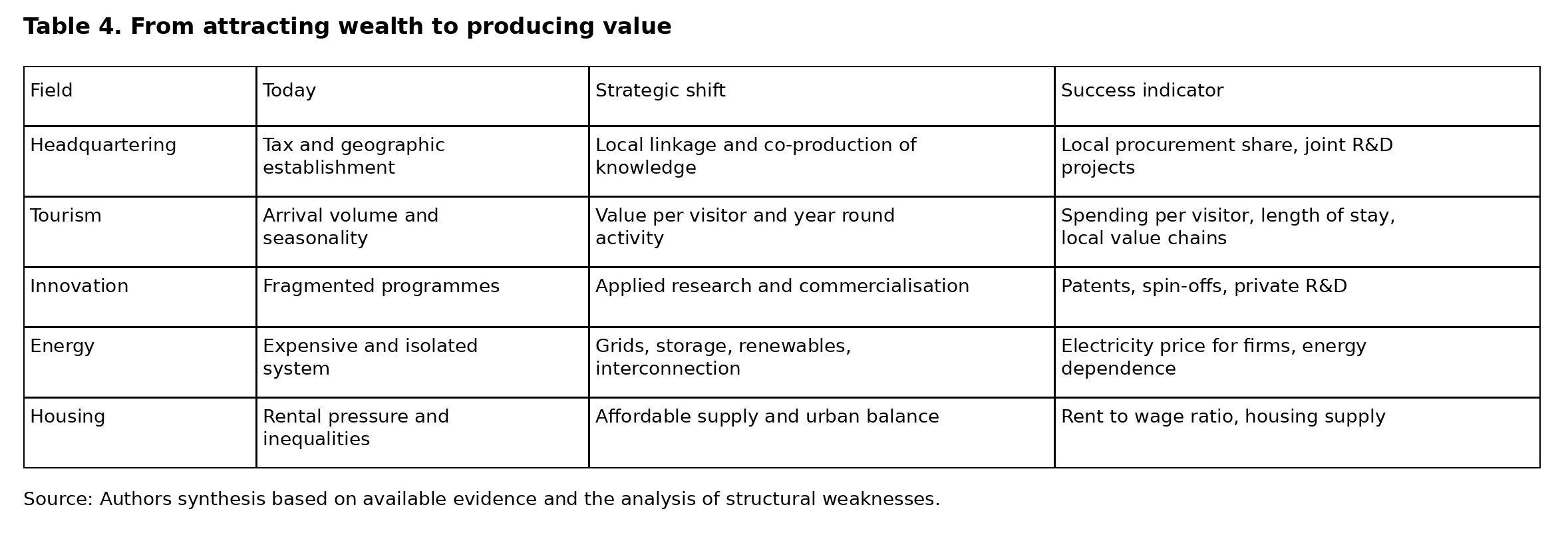

8. A new productivity contract

Cyprus needs a new productivity contract. Not another generic growth narrative, but a concrete framework that connects taxation, education, energy, universities, SMEs, technology and housing around a single objective: more domestic value added.

First, the strategy of attracting foreign companies must enter its second phase. Establishing headquarters is not enough. Cyprus needs incentives for local procurement, joint research projects with Cypriot universities, corporate laboratories, training programmes for Cypriot workers and mechanisms that connect multinationals with SMEs.

Second, tourism must move from a volume model to a value model. The country does not simply need more arrivals. It needs higher spending visitors, better spatial and seasonal distribution and stronger links to agri-food, culture, health, education and conferences.

Third, innovation policy must become less grant driven and more industrial. Grants make sense only when they lead to patents, products, spin-offs, exports and productivity. Evaluation must focus on results, not procedures.

Fourth, energy policy must be treated as development policy. Without cheaper, cleaner and more reliable energy, Cyprus will continue to pay an invisible competitiveness cost in every kilowatt-hour.

Fifth, housing must be placed at the core of economic strategy. There is no sustainable growth when young professionals, families and the middle class cannot live close to their workplaces. Real estate cannot be only an investment product. It is also productive infrastructure.

Conclusion: next success must be productive

The Cypriot economy is not in crisis. It is, however, at a demanding point of maturity. Fiscal discipline, investment grade status, low unemployment and growth close to 3 per cent are important achievements. They should not be downplayed. But they should not be misread as proof that the productive model has already been transformed.

The real question for Cyprus in 2026 is not whether it can continue to grow. It is whether it can grow differently: with more domestic value, less income leakage, a stronger technological base, lower energy costs, housing balance, value tourism rather than only volume and universities and firms that do not merely coexist in the same country but jointly produce the next productive model.

The next Cypriot success will not be measured only in GDP points. It will be measured by how much value is produced, how much value remains and how much value becomes genuine social prosperity.

Key sources, note on data

This article synthesises the three working texts and the accompanying artifact with tables and figures. Numerical values are presented as a combination of official statistics, forecasts and authors processing. Forecasts for 2026 and 2027 should be read as the estimates available at the time of writing.

- European Commission, Economic Forecast for Cyprus, Autumn 2025.

- European Commission, Country Report Cyprus 2025 and In-Depth Review under the European Semester.

- Central Bank of Cyprus, External Statistics and Balance of Payments data for 2025.

- Statistical Service of Cyprus and Gov.cy, Tourism Statistics 2025.

- Eurostat, Electricity price statistics, second half of 2025.

- Eurostat, R&D expenditure statistics, 2023 and 2024 updates.

- European Commission, European Innovation Scoreboard 2025, Cyprus country profile.

- European Commission, Education and Training Monitor 2025, Cyprus.

- European Commission Cyprus Representation, Recovery and Resilience Facility payment updates, March 2026.

- Reuters, Great Sea Interconnector updates, 2025 and 2026.

Click here to change your cookie preferences